It’s the game of making cash grow and private equity companies are in it for the long run (or at least up until they reach their rate of return, then they’re gon na sell).

Their efficiency matters both for investors and the larger economy MOST APPARENTLY noise stewards of capital were revealed to be anything but during the 2007-09 monetary crisis. Bank employers were shown to have actually taken on too much danger. Star hedge-fund managers suffered losses. Nor have the years ever since been kind. obtained $ million.

The private-equity (PE) market has been an exception to the trend. The funds it deployed during the crisis in 2007-09 have ended up yielding a mean annualised return of 18%. And it has ended up being even more important. Investors, from university endowments to public pension funds, have handed over ever more cash to PE managers (see chart).

Assets under management have inflamed to more than $4trn. The 8,000 companies run by PE in America account for 5% of its GDP, and a similar share of its labor force. Now another savage economic downturn is in full speed and the performance of PE is a sixty-four-thousand-dollar question for investors and the economy.

Specific funds can have their own timelines, financial investment goals, and management philosophies that separate them from other funds held within the same, overarching management firm. Effective private equity firms will raise lots of funds over their life time, and as companies grow in size and complexity, their funds can grow in frequency, scale and even specificity. To find out more about private equity and also - check out the websites and -.

Tyler Tysdal is a long-lasting entrepreneur helping fellow entrepreneurs sell their service for optimum value as Managing Director of Freedom Factory, the World’s Best Business Broker located in Denver, CO. Flexibility Factory assists entrepreneurs with the most significant deal of their lives.

On the other hand they have collected $1.6 trn in dry powder that they can deploy on new deals. PE stores’ fate depends upon whether the hit to their existing investments is nasty enough to clean out the possible gains from dealmaking paid for by the crisis. Start with the possible losses. In the first quarter of 2020 the four large listed PE firms, Apollo, Blackstone, Carlyle and KKR, reported paper losses on their portfolios of $90bn.

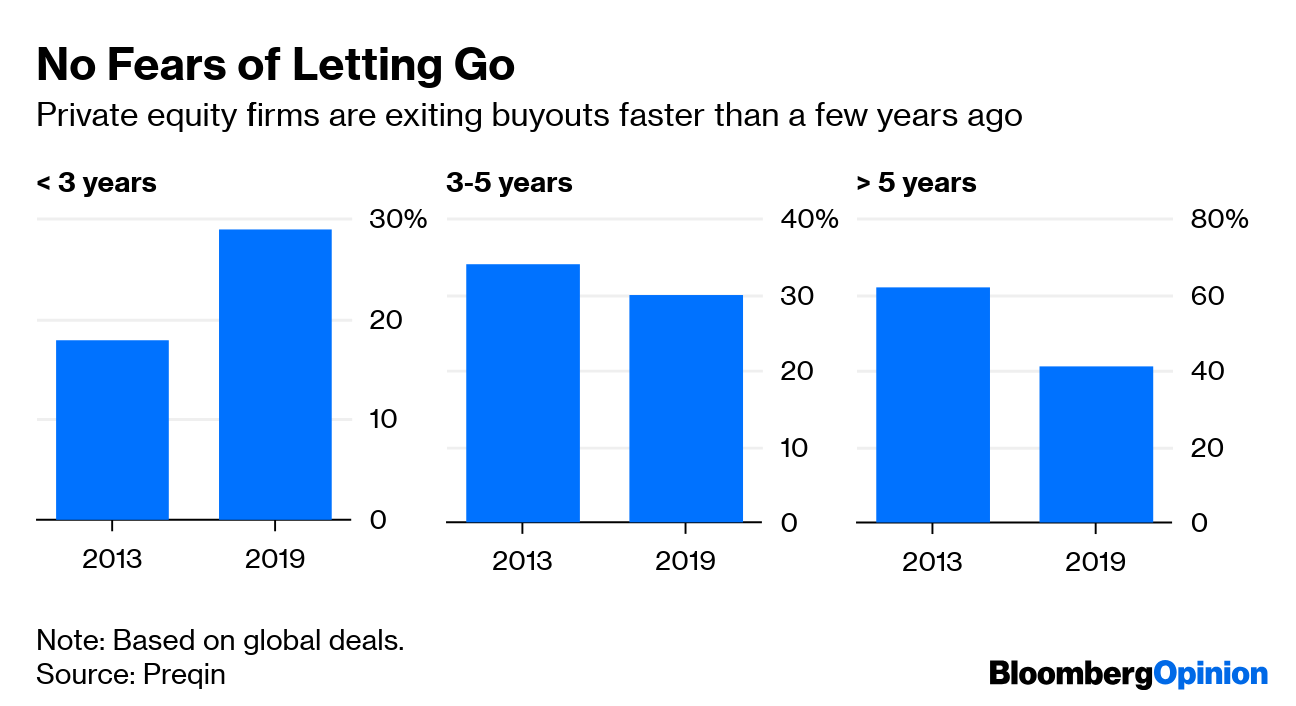

After an early scare PE companies’ investors have actually concluded that the outlook is fairly brilliant (see chart). Are they right? Numerous PE managers have been juicing up returns by piling debt on to the business they purchase. In the years instantly after the last crisis most buy-out deals were finished with financial obligation worth no more than six times gross running profits.

That would recommend that PE-run firms are susceptible. Majority of the 18 junk-rated companies that defaulted in the first quarter of the year were PE-owned, according to Moody’s, a rating company. It anticipates the general junk default rate to triple to 14% by 2021 (commit securities fraud). Over the past years PE loaning has shifted away from dopey, distracted banks towards professional private-credit firms.

Private Equity Funds – Investor.gov

And making things trickier still, most big PE supervisors say that the companies they own are either disqualified for, or unwilling to tap, the American federal government’s business bail-out schemes, the Paycheck Defense Program and the Main Street Loaning Program. However, several other aspects might have changed to work in PE’s favour.

Considering that the 2007-09 crisis numerous PE managers have actually also set up substantial credit armsfor the huge 4 firms, these now represent a 3rd of their assets. They may offer managers more internal competence and systems for raising debt, making it simpler to reorganize the financial obligations of vulnerable portfolio companies on beneficial terms.

” There is a problematic gap,” says Marc Lipschultz, co-founder of Owl Rock, a private-credit fund. “We don’t know how deep or how wide it is, however funds need to discover a bridge throughout. nfl free agent.” And if PE-run firms can not raise more financial obligation, default or reorganize their borrowings, the staying option is an “equity treatment”: PE stores stump up the money to keep their companies afloat.

The way funds are structured means that supervisors can not deploy their “dry powder” raised for brand-new funds into firms owned by older ones. state prosecutors mislead. However most older funds do have big reserves. Michael Chae, the primary monetary officer of Blackstone, says that around $30bn of its $152bn of dry powder is reserved for them.

Normally, a PE fund returns cash to its investors as soon as it sells its stake in a companybut if the financial investment duration is still ongoing, the fund can ask for it back. According to a market body for PE investors, the number of require such “recycled capital” has risen. Bailing out existing investments will drag down returns for PE shops.

The majority of PE managers hope to utilize their freshly expanded credit arms to scoop up bombed-out loans and bonds with collapsed pricesLeon Black, the founder of Apollo, has said the chance is “huge”. However the volume of standard buy-outs dropped sharply in March, and just a couple of firms have actually considering that made purchases.

Now it is time to attack. Editor’s note: A few of our covid-19 protection is free for readers of The Financial expert Today, our day-to-day newsletter. For more stories and our pandemic tracker, see our coronavirus centerThis post appeared in the Financing & economics area of the print edition under the heading “More money, more issues”.

A Beginner’s Guide To Private Equity – Entrepreneur

As Warren Buffett stated, “Rule number one: Never lose money. Rule number two: Never ever forget guideline number one.” Whether you are the CEO/founder of a start-up or an older, privately held organisation, there might come a time where you and your coworkers are looking for outdoors capital. In an ideal world, you are doing so to grow and scale a business due to demand.

Whatever the case might be, your project to raise outside capital will unquestionably involve advanced investors like private equity investors deeply inspecting your existing finances and possible to use an attractive return (civil penalty $). Essentially, if you are considering outdoors capital from private equity investors, you need to ask yourself one vital question: “Is my organisation all set for the demands of private equity?” As the president of a nationwide executive search firm, I routinely stumble upon situations where private equity firms are applying significant pressure on their portfolio companies to adhere to greater performance requirements.

A number of these circumstances require us to replace the existing CFO with a private equity knowledgeable prospect. So why do private equity firms do this? As mentioned by Buffett, it is to safeguard their financial investment. Specifically if the private equity firm is investing 8 or 9 figures into your company, the stakes are exceptionally high.

Specifically, I will discuss some substantial modifications in terms of reporting standards and workers that private equity firms require of portfolio business. Regardless of the funding source, business that get outdoors capital are having fun with raised stakes. Lax compliance standards or incomplete monetary statements are merely out of the question.

Frequently, portfolio business offer this clearness through more in-depth monetary statements – denver district court. In fact, this increased level of information may be an obligatory part of the fundraising round. As simply one example, many private equity companies require their portfolio companies to have a tough close on a monthly basis. Many private companies forego this practice every month, instead selecting to do it every quarter or every year.

If the portfolio business does not have the resources to quickly execute a month-to-month close, it might create some substantial obstacles within the organization. Along with a monthly hard close, private equity companies typically institute strict financial planning and analysis (FP&A) requirements. These FP&A requirements may include things like cash flow projections, EBITDA (revenues prior to interest, tax, depreciation and amortization) bridges and more.